Background

Description

This repository implements a production-style quantitative valuation pipeline for equity options, combining high-performance pricing models with a full data and calibration workflow.

The system goes beyond a standalone pricer: it integrates market data ingestion, structured storage, numerical pricing, and volatility surface calibration into a single reproducible framework.

The goal of this project

The goal of this project is to serve as a modular foundation for quantitative modeling and experimentation in option pricing and financial time series.

Mathematical Framework

Read about what the option pricing engine actually does → Option Pricing Engine Mathematical Framework

Roadmap

The roadmap is outlined in the following flow chart

.png)

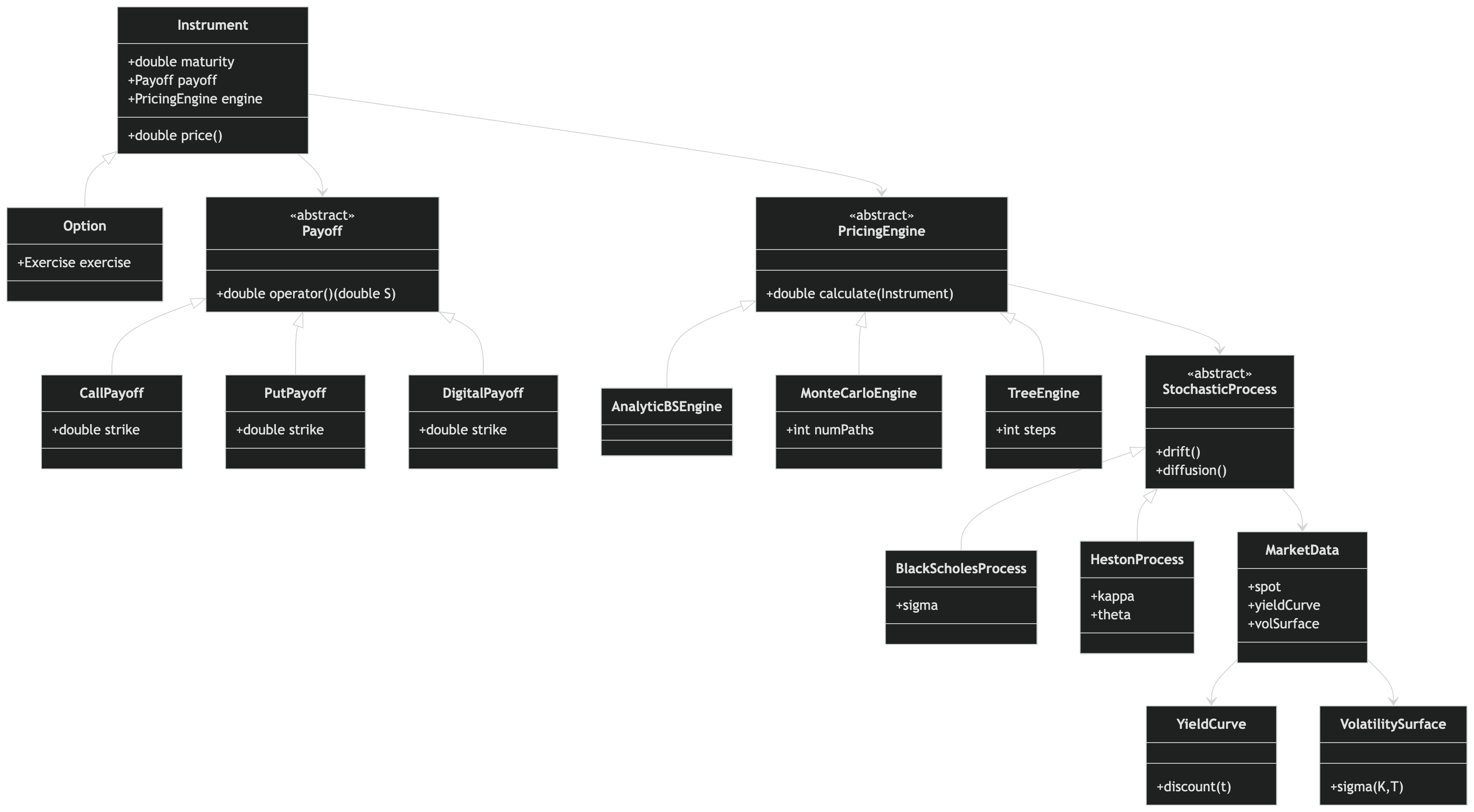

Design

Rough planned class diagram sketch for qengine

📊 Observations and further analysis

- Find out how the implied volatility was reconstructed from real world market data using this system and what challenges were faced along the way: → Option Price Engine Implied Volatility Analysis

- Investigate research based techniques how to compute the local volatility from the implied volatility surface data: → Local volatility computations

Bonus projects

- Realize a battery storage optimization schedule based on a real-world timeseries of electricity prices. → Battery Storage Optimization

Testing strategy

Unit tests

- Payoff

- Black-Scholes Process unit test

- Test with a given result

- Random number generator tests

- Statistics unit tests

Written by David Doebel 03.04.2026 LinkedIn: https://www.linkedin.com/in/david-doebel-b1b9b1339/