Market data suggests that the fair price of an option does not depend on a constant volatility , but rather on a volatility that varies with strike and maturity . In the previous section, we fitted this dependence by a smooth implied volatility surface, obtained by inverting the Black—Scholes pricing formula for observed market prices. Based on this surface, it is possible to recover the local volatility via Dupire’s formula:

[@gatheralVolatilitySurfacePractitioners2006], Eq. 1.6

Defining the implied total variance

and the log moneyness

where denotes the forward price at maturity , Dupire’s formula can be rewritten in terms of the total variance surface as

[@gatheralVolatilitySurfacePractitioners2006], Eq. 1.10

Computational issues

The practical difficulty of this formula is its severe numerical instability, since it involves first- and second-order derivatives of the fitted variance surface. We illustrate this by a simple numerical experiment.

Let

Then the corresponding derivatives are

Substituting these expressions into Dupire’s formula yields the analytic local variance

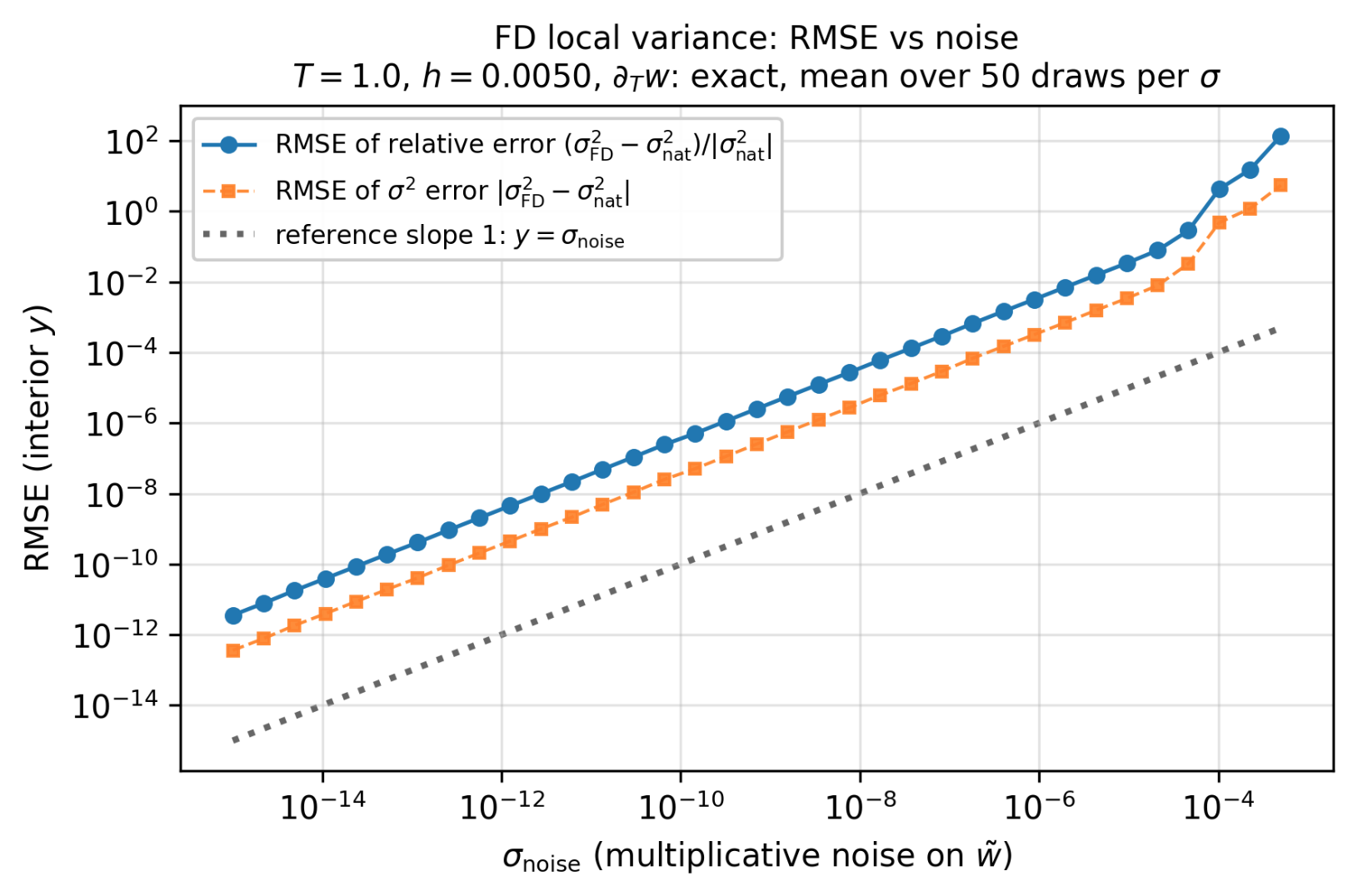

To mimic the effect of noisy market calibration, we perturb the total variance on a discrete grid . Specifically, we define a noisy approximation

where the are independent.

Assuming a uniform grid with spacing , the derivatives of are approximated by central finite differences:

and

Using these finite-difference approximations in Dupire’s formula produces a noisy estimate of the local variance. Empirically, the resulting error scales approximately linearly with the noise level , as shown in Figure 1. This demonstrates that the map from the implied variance surface to the local volatility surface is highly ill-conditioned: even small perturbations in can lead to large errors in the recovered local volatility.

References

J. Gatheral, The Volatility Surface: A Practitioner’s Guide. Wiley Finance Series. Hoboken, NJ: John Wiley & Sons, 2006. doi: 10.1002/9781119202073.